In this third instalment of our thought leadership series on disruptive innovation, we examine how disruption has played out in the unique South African context. Building on our previous exploration of the theoretical foundations of disruptive innovation (Part 1) and business model innovation (Part 2), we now turn to real-world evidence from homegrown success stories and failures. Analysing the way Capitec Bank transformed its market, how Discovery Health designed an innovation around behaviour, and the difference in fortunes between ride-hailing and mobile money, provides powerful frameworks entrepreneurs and corporates can use to innovate in Africa.

When Capitec Bank was launched in 2001, the South African banking sector was a fortress. The four incumbents controlled 80% of the retail market (Publishing London Business School, 2017). Many traditional banks have built their retail banking businesses around complex products, high fees, and segmentation. Millions of lower-income South Africans were left behind or inadequately served because they were viewed as unprofitable using standard metrics.

Capitec Bank’s founders recognised an opportunity where competitors saw only risk. They had a simple yet disruptive idea: make banking accessible, affordable and intuitive. Capitec Bank’s Global One account maintained transparent pricing, no hidden fees, the R5 monthly maintenance cost was straightforward, unlike the numerous fees in traditional banking. This was not just a pricing scheme, but rather a business model innovation that challenged key industry beliefs about customer profitability.

Capitec Bank’s financial transformation suggests disruptive innovation has taken place. Capitec’s headline earnings amounted to R13.739 billion in 2025, which is a 30% growth from the previous year (Capitec Bank Holdings Limited, 2025a). Even more impressive, the bank now serves more than 25 million clients, which is more than half of South Africa’s adult population. The significant expansion transpired with stellar operational efficiency marked by a cost-to-income ratio of 38%, which is noteworthy when compared to the industry average of 56%.

Examining Capitec’s diversified ecosystem reveals the extent of this change. According to Capitec Bank Holdings Limited (2025b), Group earnings were bolstered by 26% from value-added services and another 26% from insurance. According to Capitec Bank Holdings Limited (2025a), Capitec Connect, the bank’s mobile virtual network operator, has 1.1 million active SIMs. Meanwhile, the bank has 3.3 million active funeral and life-cover policies, insuring 15 million lives.

Capitec was unique for three reasons. Initially, they developed digital infrastructure from the ground up, rather than layering technology onto legacy systems. Currently, 14 million clients use their mobile app today, accounting for 88% of digital transactions (Capitec Bank Holdings Limited, 2025b). Secondly, they stripped back non-essential functions at branches, pushing customers into digital channels while maintaining a physical presence in shopping centres where people feel comfortable. Third, they implemented a sustainable flywheel where improved operating efficiency lowered costs in order to fund customer acquisition and platform expansion.

South Africa’s economy benefited from its ecosystem strategy. Although fees were cut and R203 million returned to clients through fee simplification in 2025, profitability was strong (Capitec Bank Holdings Limited, 2025b). The lesson is clear: a new business model can create access to unmet needs and unlock previously unreachable customer segments.

In 1992, Adrian Gore founded Discovery with an insight which challenged one of the core assumptions of insurance: that risk is static. Traditional insurers treated policyholders as fixed risk profiles with little incentive to change health outcomes. The Vitality programme, which launched in 1997, reversed this model via behavioural economics.

The shared-value strategy promotes healthy behaviour with real-world rewards. Members undergo health assessments, earn points for going to the gym, exercising and buying healthy food, and receive attractive benefits of up to 100% off on gym fees, 75% off on international flights, and huge fuel cashbacks. The insurer profits by receiving fewer claims, while customers enjoy better health and finances.

Discovery’s financial results for 2025 demonstrate the effectiveness of the model, as the headline earnings rose by 30% to R9.625 billion, while normalised operating profit rose by 29% to R15.210 million (Discovery Limited, 2025a) The Vitality model is present in more than 40 markets through the Global Vitality Network, with over 40 million members worldwide (Discovery Limited, 2025a).

Discovery’s innovation extends beyond simple incentives to sophisticated data utilisation. The firm has amassed 40 million life years of morbidity and mortality data, revealing that active Vitality members live, on average, 11 years longer and incur 21% lower lifetime health care costs (Discovery Limited, 2025a). In 2025, the Group used AI for risk and engagement transformation, launching Vitality AI as Personal Health Pathways (Discovery Limited, 2025a). The large quantity of relevant data enabled the emergence of network effects that competitors cannot easily duplicate. Discovery Bank, which was reported by Discovery Limited (2025b) to be the world’s first “behavioural bank”, reached monthly break-even ahead of plan and achieved its first period of profitability during the second half of 2025, largely due to its Vitality ecosystem enabling entry into adjacent markets.

Overall, the key takeaway here is not just in health care: successful disruptors often don’t just innovate their product, but rather they innovate and influence the value network around it. The integration of healthcare, finance, and retail solutions into one platform ultimately gave Discovery competitive advantages that rivals could not plug into overnight.

Start-ups aren’t the only ones that disrupt. When Checkers, which is owned by Shoprite, launched Sixty60 in November 2019, they collaborated with South African technology start-up Zulzi. Their proposition is elegantly simple: groceries ordered in 60 seconds are delivered in 60 minutes (SAP Africa News Centre, 2024).

The timing of this launch proved to be lucky as the orders went up drastically due to COVID lockdown. As of March 2025, Sixty60 had grown sales by 47.1%, with more than 601 stores offering the service (Joburg ETC, 2025). The platform is now estimated to generate R10 billion per year, commanding more than 80% market share of on-demand grocery delivery in South Africa (Daily Investor, 2024).

Sixty60 stands apart from global competitors for its operational excellence and capital efficiency. Instead of building costly, publicly ‘hidden’ distribution centres, Checkers uses existing stores as micro-fulfilment centres. Deliveries hit 94% on-time rates and 97% order fulfilment, while the claim by CEO Pieter Engelbrecht, who said “it is very profitable”, makes the service different from most on-demand services globally (Daily Investor, 2024).

The platform’s inception has generated almost 14,200 job opportunities, showing that incumbents with the right strategy, technology partnerships, and execution capabilities can lead disruption, not follow it (Wikipedia, 2025). The lesson: existing players can win if they leverage established assets rather than simply copying start-ups’ models.

Uber made its South African debut in Johannesburg and Cape Town in 2013, making ride-hailing available in a market with few metered taxis and route-based minibus public transport. The value proposition was strong: convenient, safe, point-to-point transport at transparent prices via smartphone apps.

Uber has had a major economic impact: in 2023, drivers and delivery couriers earned R2.3 billion via the platform in South Africa, with an estimated R17 billion economic impact in the country (ITWeb, 2024b). This represents 3.5% of total economic output for the transport sector, which supports an estimated 135,000 gig workers (Public First & Uber, 2024). However, some turbulence was experienced along the way. The absence of regulation sparked violent clashes with taxi drivers, with cars burned and drivers attacked. It wasn’t until the National Land Transport Amendment Act of 2023 that e-hailing services received any official recognition and regulatory clarity after nearly a decade of limbo (Knowledge Sourcing Intelligence, 2025).

The platform has been adapted for South African conditions. Due to high crime rates, safety features such as panic buttons and trip sharing became a necessity, whilst payment in cash addressed financial inclusion gaps. In 2023, Uber’s additional value creation for the tourism industry was estimated at R1 billion (Public First & Uber 2024). However, challenges remain. Driver surveys reveal that many forfeit 65% of earnings to fleet partners and fuel costs, whilst drivers earn less than the minimum wage of R27.58 per hour, according to industry analysis (Daily Maverick, 2025). Emerging markets create distinctive hurdles for global disruptive models, which require major local adaptations.

Insights from M-Pesa’s failure in South Africa underscore the context-dependence of disruption. Initially launched in Kenya, M-Pesa is a mobile phone-based money transfer, payments and micro-financing service. Despite being a tremendous success in Kenya, where it processes $50 billion a year and has 40 million users, Vodacom’s South African M-Pesa had only 76,000 active users and was discontinued in 2016 (Goldstuck, 2016).

The mistake was thinking that Kenya’s playbook would translate directly to South Africa. When M-Pesa was launched in Kenya, only 20% of the population were using banking services, whilst in South Africa, banking penetration was already 75% (Goldstuck, 2016). Importantly, millions of users were already engaged with FNB eWallet, while Shoprite offered money transfers for R1. The pressing need which drove Kenyan adoption simply didn’t exist in South Africa.

There were also challenges associated with distribution, coupled with different socio-political conditions, in South Africa. Notably, Kenya had 60,000+ agents, while South Africa launched with insufficient coverage (ITWeb, 2024a). Perhaps most importantly, regulatory requirements forced partnerships with established banks in South Africa, which created friction and increased costs. This was in contrast to Kenya’s initially more permissive environment. In addition, the violence following the 2007-2008 elections in Kenya caused a spike in the demand for remote money transfer that did not exist in South Africa (Goldstuck, 2016).

The M-Pesa failure highlights three success factors of mobile money: demand due to financial exclusion from traditional banking processes, regulation to support rapid scaling, and crisis events to spur fast scaling. This case shows that well-funded, technically proven innovations can fail when assumptions about context are wrong. According to one analyst, Vodacom “never really listened to outside advice, they assumed their Kenyan experience qualified them in South Africa, and it was quite the opposite” (Goldstuck, 2016).

Analysing these case studies requires taking an in-depth look at South Africa’s distinctive innovation ecosystem, which is characterised as having mobile-first adoption, regulatory sophistication and very high levels of inequality.

The mobile-centric infrastructure in South Africa has opened up opportunities for leapfrog solutions, with e-hailing being valued at almost R7-billion (Knowledge Sourcing Intelligence, 2025). Nonetheless, on the design side, the contextual nuances also mean that solutions need to work on low-end Android devices with patchy 3G connectivity and stay cost-effective for data-sensitive users.

Within this context, disruptors who are successful exhibit ingenuity, which includes features like fintech apps that offer USSD options, charging stations in townships that use solar power, as well as offline functionality for when connectivity is unreliable. A critical lesson is that mobile-first doesn’t mean smartphone-only, but rather, inclusive design in this context means that multiple access points are required.

South Africa’s regulatory mechanisms favour cooperation over conflict. Capitec received a full banking licence and complied with capital regulations, opting to disrupt from within the system. Discovery successfully operated in accordance with insurance legislation while lobbying for recognition of its incentives model. Recent initiatives, such as the fintech sandbox, demonstrate regulatory willingness to innovate, whilst simultaneously maintaining stability. In South Africa, the strategic imperative is clear: engage with the regulators early, clearly demonstrate alignment with national priorities, including financial inclusion and job creation, and build compliance into innovations rather than making it an afterthought.

The high levels of inequality in South Africa present both opportunity and obligation for inclusive innovation. Learning from the above case studies, Capitec profited from serving lower-income customers on a large scale. According to Public First and Uber (2024), 135,000 gig workers or 1% of the employed population generated an income through Uber-like platforms. Although it targeted the middle class, Discovery’s model had broader societal health benefits.

In the South African context, the pattern is unmistakable: when profit and social impact are aligned, innovations tend to be more widely accepted in the marketplace, last longer and have a bigger impact. In a country with around 32% unemployment, if an innovation can empower people economically, it significantly enhances its chances of success.

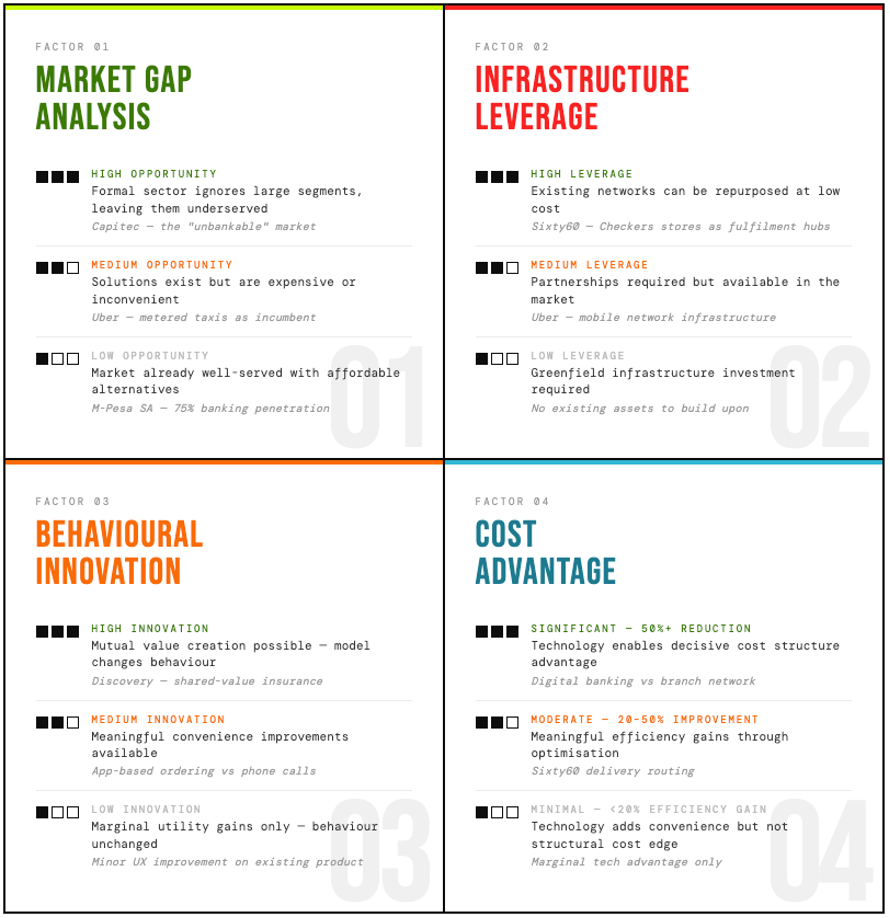

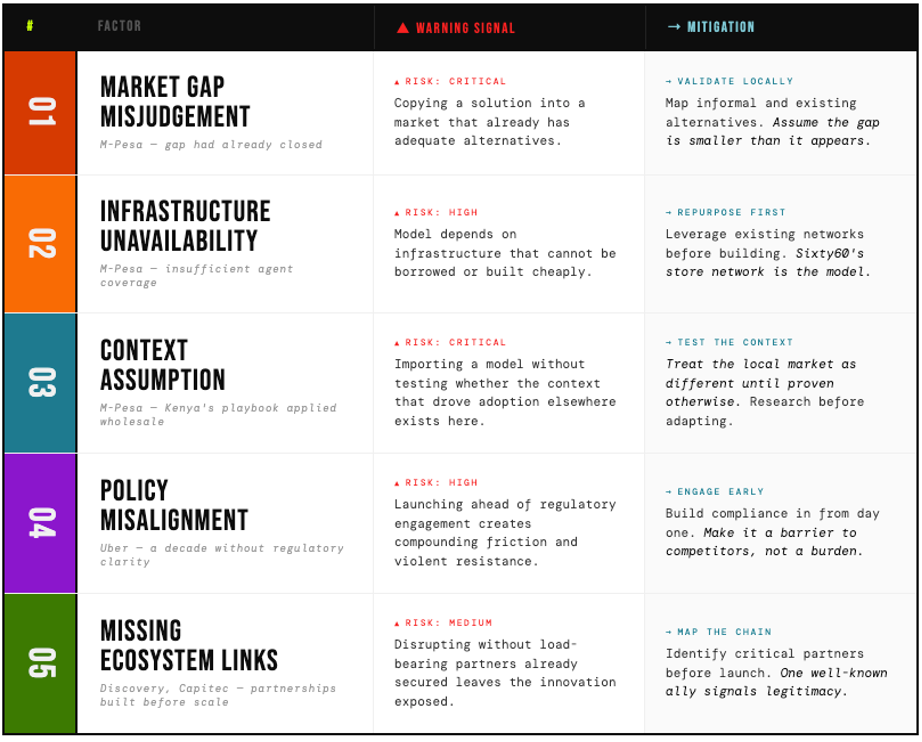

The five cases examined in this article – Capitec, Discovery, Sixty60, Uber, and M-Pesa – are not simply inspiring stories. Read together, they form a coherent pattern. Each success shares a common anatomy: a clearly identified gap that incumbents had ignored or mispriced, existing infrastructure repurposed rather than rebuilt from scratch, a business model that changed behaviour rather than merely replicated it, and a cost structure that technology made decisively more efficient. Each failure, meanwhile, reflects the absence of at least one of these conditions. M-Pesa arrived in a market where the gap had already closed. Context was assumed rather than tested. The need that drove Kenyan adoption simply did not exist here.

These patterns suggest a practical diagnostic – a way of stress-testing any innovation opportunity before committing capital and energy to it. We call this the Four-Factor Opportunity Assessment.

Scoring well across all four dimensions does not guarantee success. The case studies also reveal five execution factors that separate innovations that scale from those that stall.

Ecosystem orchestration is perhaps the least intuitive but most consistently decisive. None of the successes here was won in isolation. Discovery built a partner network spanning gyms, retailers, airlines, and eventually banks. Sixty60 drew on a technology start-up for what Checkers could not build internally. Capitec integrated insurance and mobile connectivity into a banking platform. The winning logic is mutual value creation – building arrangements where partners have a genuine incentive to make the ecosystem grow, rather than competing for a fixed share of it.

Regulatory engagement emerges as a competitive advantage in disguise. Capitec and Discovery both worked within the regulatory framework while subtly reshaping it. Uber’s decade in regulatory limbo was costly in ways that went beyond legal fees – it constrained driver certainty, deterred institutional partners, and invited violent resistance. The strategic implication is clear: engage regulators early, demonstrate alignment with national priorities such as financial inclusion and job creation, and treat compliance as architecture rather than an afterthought.

Inclusive business model design is not a social nicety in the South African context – it is a commercial logic. Capitec’s 25 million clients did not exist as a bankable market until Capitec created the conditions for them. With around 32% unemployment and a Gini coefficient among the highest in the world, the mass market in South Africa is the lower-income market. Innovations that serve only the affluent segment are structurally limited in their scale.

Mobile-first, context-aware design requires a more honest interpretation than the phrase usually receives. Mobile-first in South Africa does not mean smartphone-first. It means designing for patchy 3G, low-end Android devices, data-sensitive users, and in many cases, USSD as a parallel access channel. The platforms that have endured – Capitec’s app serving 14 million clients, Sixty60’s seamless checkout – have done so by treating these constraints as design requirements rather than exceptions.

Local adaptation is the lesson M-Pesa teaches most directly. Proven models imported wholesale from other contexts carry hidden assumptions – about infrastructure density, about what competing solutions already exist, about the socio-political triggers that drove adoption elsewhere. A useful rule of thumb: always assume the context is different until it can be demonstrated otherwise.

These five factors are not a checklist. They interact. Regulatory engagement without inclusive design produces compliant but narrow innovations. Ecosystem orchestration without mobile-first thinking produces platforms that only the already-served can access. The strongest innovations in this article scored well across all five simultaneously.

The disruptive landscape in South Africa continues to evolve. The next wave of innovation will be shaped by several trends.

The pattern that runs through every case in this article is more precise than “innovate boldly” or “move fast.” It is this: in a high-inequality, mobile-first, resource-constrained context, the innovations that endure are those where commercial logic and social impact point in the same direction. Capitec did not serve the “unbankable” market out of obligation – it did so because the incumbents had mispriced the opportunity. Discovery did not improve public health as a side effect of its business model – improved health was the mechanism through which it reduced claims and grew revenue. Sixty60 did not create 14,200 jobs incidentally – job creation was the operational infrastructure that made 60-minute delivery possible. When disruption is designed for inclusion, it does not sacrifice commercial performance. It compounds it.

South Africa’s 0.63 Gini coefficient is not only a measure of inequality – it is a map of where the largest underserved markets sit. The frameworks in this article are tools for reading that map. For entrepreneurs and corporates alike, the Four-Factor Assessment and the Failure Prediction factors are not theoretical – they are drawn directly from the decisions that made Capitec, Discovery and Sixty60 what they are today, and from the assumptions that made M-Pesa’s South African chapter a cautionary tale. The invitation is straightforward: stress-test your opportunity against these patterns before committing capital, build compliance and inclusion into the architecture of your model rather than bolting them on afterwards, and treat South Africa’s structural constraints not as obstacles to work around, but as the precise conditions that make locally-grounded innovation defensible at scale.

Capitec Bank Holdings Limited. (2025a, April 23). Headline earnings grow by 30%. Retrieved from https://www.capitecbank.co.za/blog/news/2025/annual-results/

Capitec Bank Holdings Limited. (2025b, October 1). Interim results: Headline earnings rising 26% to R8 billion. Retrieved from https://www.capitecbank.co.za/blog/news/2025/interim-results/

Daily Investor. (2024, March 6). Checkers Sixty60 revenue estimate – and it is eye-wateringly high. Retrieved from https://dailyinvestor.com/retail/46201/checkers-sixty60-revenue-estimate-and-it-is-eye-wateringly-high/

Daily Maverick. (2025, March 4). Uber drivers and the exorbitant cost of working in the gig economy. Retrieved from https://www.dailymaverick.co.za/article/2025-03-03-uber-drivers-an-exorbitant-cost-of-working-in-gig-economy/

Discovery Limited. (2025a, September 11). Discovery Group delivers strong annual performance as it enters a distinct new growth phase with two well defined operational composites. Retrieved from https://www.mynewsdesk.com/za/discovery-holdings-ltd/pressreleases/discovery-group-delivers-strong-annual-performance-as-it-enters-a-distinct-new-growth-phase-with-two-well-defined-operational-composites-3404011

Discovery Limited. (2025b, March 4). Discovery’s new phase of growth results in strong performance, with Discovery Bank continuing to perform ahead of plan. Retrieved from https://www.mynewsdesk.com/za/discovery-holdings-ltd/pressreleases/discoverys-new-phase-of-growth-results-in-strong-performance-with-discovery-bank-continuing-to-perform-ahead-of-plan-3373143

Goldstuck, A. (2016, May 9). Why Vodacom M-Pesa has flopped in SA. News24. Retrieved from https://www.news24.com/business/tech/companies/why-vodacom-m-pesa-has-flopped-in-sa-20160509

ITWeb. (2024a, May 19). What went wrong for M-Pesa in SA. Retrieved from https://www.itweb.co.za/article/what-went-wrong-for-m-pesa-in-sa/lP3gQ2MG2897nRD1

ITWeb. (2024b, December 9). Uber SA drivers, couriers earned R2.3bn in 2023. Retrieved from https://www.itweb.co.za/article/uber-sa-drivers-couriers-earned-r23bn-in-2023/4r1lyMR9plQ7pmda

Joburg ETC. (2025, March 4). Checkers Sixty60 expansion: How it’s changing retail in South Africa. Retrieved from https://www.joburgetc.com/business/checkers-sixty60-expansion-south-africa/

Knowledge Sourcing Intelligence. (2025, September 12). South Africa E-hailing market report: Trends, forecast 2030. Retrieved from https://www.knowledge-sourcing.com/report/south-africa-e-hailing-market

News24. (2024, October 1). Capitec reports 36% headline earnings growth to R6.4 billion. Retrieved from https://www.news24.com/brandstory/partner-content/capitec-reports-36-headline-earnings-growth-to-r64-billion-20241001

Publishing London Business School. (2017). Capitec Bank: David and Goliath in South African banking. London Business School Case Study.

Public First & Uber. (2024). Uber South Africa economic impact report. Retrieved from https://ubersouthafrica.publicfirst.co/

SAP Africa News Center. (2024, September 2). The people behind South Africa’s biggest on-demand grocery delivery service. Retrieved from https://news.sap.com/africa/2024/09/the-people-behind-south-africas-biggest-on-demand-grocery-delivery-service/

TechCentral. (2025, March 4). Checkers Sixty60 still pumping, but sales growth is slowing. Retrieved from https://techcentral.co.za/checkers-sixty60-still-pumping-slowing/260109/

Wikipedia. (2025). Checkers (supermarket chain). Retrieved from https://en.wikipedia.org/wiki/Checkers_(supermarket_chain)

Note: All financial figures are in South African Rand unless otherwise specified. Exchange rates and comparative data are current as of December 2025.